Introduction to tax on share schemes (part 1)

Tax Advice » August 1, 2024

If your clients have complex remuneration in the form of shares, options or RSUs these can be hard to value and can be difficult to arrive at the after tax figure for the options. As with other income share values are often provided gross (i.e. before tax has been deducted and as income tax as well as capital gains tax applies to shares.

This is a short introduction to understanding share schemes on divorce;

The first step is know what type of shares or options they are. There are two categories of shares.

- Approved schemes = tax efficient

- Non tax approved schemes = regular tax rules apply

Employees generally get shares in their employer’s company in one of two ways:

1. through an award of shares by the employer

2. on the exercise of a share option

In simple terms, shares have;

| An award date | the date they are promised to the employee |

| A vest date | the day the employee owns the share |

| A sale date | when the employee sells the share |

Share options are the right to acquire to shares in the employer company in a given period of time they have;

| A grant date | the date the employee is given the opportunity to purchase options at a certain price |

| An exercise date | the date the employee chooses to exercise this right, eg the date they buy the option at the agreed price |

| A sale date | when the employee sells the options |

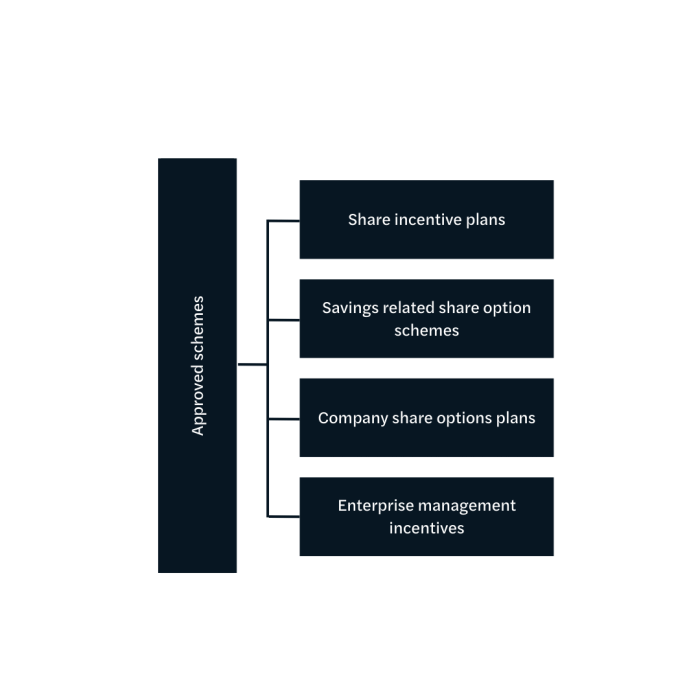

There are four main types of tax advantaged share scheme which have tax and NIC advantages; they are:

If your client has shares in one of the above schemes then the treatment of the shares will be tax advantaged. A summary of how the shares will be taxed is below:

| Share scheme | Conditions | Tax Treatment |

| Share Incentive Plans (SIPs) | Free and matching shares must be subject to a holding period of between 3 and 5 years (unless employment ceases) | Share is free from income tax if withdrawn after 5 years. Income tax charge if withdrawn early Capital gains tax is charged on the sale prices less the value of the share when it left the plan |

| Savings related share option schemes | Employees must save between £5 to £500 per month for either 3, 5 or 7 years. The price of the option must be at least 80% of the open market value | No income tax Only capital gains tax is payable on disposal |

| Company Share Options (CSOPs) | No discounts allowed at grant. Maximum value at grant is £30,000 Must be held for between 3 and 10 years | Income tax on exercise if outside the 3 to 10-year period. Capital gains tax on disposal |

| Enterprise Management Incentives | Must be full time employees Option must be exercised | Income tax on exercise if the options were given at a discount or if exercised >10 years from grant |

When seeking a tax report on approved plans you will need to provide the following

- Award Agreement

- Share plan agreement

- Vesting schedule

You may need to know both the income tax and future capital gains tax position now and if the shares are retained for their minimum period per the terms.

Part two of this series will talk through the share award life cycle for unapproved shares including RSUs.

Sign up to be notified when we publish new articles: Juno Family Newsletter

Need expert tax support?

Find a full list of how Juno can support on our Services page. Alternatively, get in touch with our team at: family@junotax.co.uk